What is a Loan Management System? (Loan Management System Kya Hota Hai?)

Agar aap ek bank, NBFC, ya kisi bhi lending company mein kaam karte hain, toh aapne yeh problem zaroor dekhi hogi.

Ek customer loan ke liye apply karta hai. Documents manually collect hote hain. Spreadsheets mein data enter hota hai. Approvals ke liye emails aate-jaate hain. Aur jab EMI miss hoti hai, toh follow-up bhi manually hota hai.

Yahi sab kuch ek Loan Management System solve karta hai.

Loan Management System (LMS) ek software platform hai jo kisi bhi lending organization ke loan processes ko start se end tak manage karta hai. Matlab loan application se lekar disbursement tak, aur disbursement se lekar final repayment tak — sab kuch ek hi system mein.

Aaj ke time mein jab India mein digital lending ka market 2026 mein 350 billion USD ke paar jaane ki expectation hai, ek robust LMS sirf ek option nahi raha — yeh ek necessity ban gaya hai.

Loan Management System Kaise Kaam Karta Hai?

LMS ek centralized platform ki tarah kaam karta hai jahan loan ka poora lifecycle track hota hai. Isko 4 main stages mein samjha ja sakta hai.

Stage 1: Loan Origination (Application Process)

Pehla step hota hai loan origination. Jab koi customer loan ke liye apply karta hai, toh LMS yeh sab handle karta hai:

- Online application form fill karna

- KYC documents upload karna (Aadhaar, PAN, bank statements)

- Credit score check karna (Credit, Experian ya CRIF se integration ke through)

- Eligibility calculation automatic hona

Pehle yeh sab manually hota tha jisme kaafi time aur errors aate the. LMS ne yeh poora process digital aur fast kar diya hai.

Stage 2: Underwriting aur Approval

Application aane ke baad system automatically risk assessment karta hai. Loan officer ko har cheez manually check nahi karni padti. LMS:

- Income verification karta hai

- Existing liabilities dekha hai

- Fraud check run karta hai

- Credit policy ke against application evaluate karta hai

Final approval human ke paas jaati hai, lekin 80 percent groundwork LMS ne pehle hi kar di hoti hai.

Stage 3: Disbursement

Loan approve hone ke baad LMS disbursement process manage karta hai:

- Loan agreement auto-generate hota hai

- E-signature collect hoti hai

- Amount bank account mein transfer hoti hai

- Repayment schedule automatically set hoti hai

Stage 4: Loan Servicing aur Collections

Yeh wo part hai jahan zyada kaam hota hai aur zyada errors bhi aate hain jab system nahi hota.

- EMI payment tracking

- Automatic reminders (SMS, email, WhatsApp)

- Late payment penalty calculation

- Prepayment aur part-payment handling

- NOC generation on full repayment

Loan Management System ke Key Features

Ek accha LMS choose karte waqt yeh features zaroor dekhne chahiye:

1. Loan Origination Module

Yeh module loan application process ko handle karta hai. Achha origination module woh hota hai jisme customer khud apni application complete kar sake, bina branch visit kiye. Mobile-friendly interface, document upload, aur real-time status tracking — yeh teeno cheezein essential hain.

2. Credit Assessment aur Decisioning Engine

LMS ka yeh part decide karta hai ki loan approve karna chahiye ya nahi. Modern LMS systems mein AI-based decisioning engines hote hain jo Credit score ke saath saath alternative data bhi consider karte hain jaise GST returns, bank statement patterns, aur even utility bill payment history.

3. Document Management System

Loan process mein documents ki bhaad aa jaati hai. Ek achha LMS document version control, OCR (optical character recognition), aur tamper-proof document storage provide karta hai. Audit ke waqt koi bhi document 2 minute mein milna chahiye.

4. EMI aur Repayment Tracking

Yeh LMS ka sabse critical feature hai. System ko automatically:

- EMI due dates track karni chahiye

- Payment received mark karna chahiye

- Pending payment reminders bhejne chahiye

- Partial payment handle karni chahiye

- Foreclosure calculation show karni chahiye

5. NPA Management (Non-Performing Assets)

RBI ke guidelines ke mutabiq, agar koi loan 90 days se zyada overdue hai toh usse NPA declare karna padta hai. LMS automatically NPA accounts flag karta hai aur recovery process initiate karne mein help karta hai.

6. Reporting aur Analytics Dashboard

Lending business mein data bahut important hai. LMS ko real-time dashboards provide karne chahiye jisse management ko pata chale:

- Kitne loans active hain

- Kitna portfolio at risk hai

- Collection efficiency kya hai

- Branch-wise ya product-wise performance kya hai

7. Regulatory Compliance (RBI, NBFC Guidelines)

India mein lending heavily regulated hai. LMS ko RBI guidelines, Fair Practice Code, aur KYC norms ke saath compliant hona chahiye. Yeh sirf legal requirement nahi hai — audit mein yeh system ki zaroorat pad jaati hai.

8. API Integration Capability

Modern LMS systems ko dusre systems ke saath baat karni hoti hai:

- Core Banking System (CBS)

- Credit bureaus (Credit, Experian)

- Payment gateways (Razorpay, PayU)

- Accounting software (Tally, SAP)

- Government databases (Aadhaar, GST portal)

Types of Loan Management Systems

LMS ek hi type ka nahi hota. Use case ke hisaab se alag-alag types hote hain.

Retail Loan Management System

Personal loans, home loans, car loans, aur education loans ke liye. Yahan volume zyada hota hai aur ticket size alag-alag. System ko scale karna padta hai.

MSME aur Business Loan Management System

SME lending ke liye alag considerations hote hain. Business financials analyze karna, GST data pull karna, aur collateral management — yeh sab features specifically business lending ke liye design honii chahiye.

Microfinance Loan Management System (MFI LMS)

Microfinance institutions ke liye specifically designed LMS hote hain jahan group lending, joint liability groups (JLG), aur field agent management important features hote hain. Offline functionality bhi zaroori hoti hai kyunki rural areas mein internet reliable nahi hota.

Agricultural Loan Management System

Kisan credit cards, crop loans, aur seasonal lending ke liye. Kharif-rabi cycles ke saath repayment schedules align karna, land records integrate karna, aur weather-based risk assessment — yeh specific features chahiye hote hain.

Vehicle Loan Management System

RC book verification, insurance tracking, hypothecation management, aur repossession workflow — vehicle loans ke liye khas features.

Loan Management System ke Fayde (Benefits)

Loan Management System vs Traditional Methods: Clear Comparison

| Parameter | Traditional Method | Loan Management System |

| Application process | Manual form, branch visit | Online, mobile-friendly |

| Processing time | 7 to 15 days | 24 to 48 hours |

| Document handling | Physical files | Digital, cloud-stored |

| EMI tracking | Spreadsheet or register | Automated, real-time |

| Credit check | Manual bureau query | API-integrated, instant |

| Reporting | Monthly, prepared manually | Real-time dashboard |

| Error rate | High | Near zero |

| Scalability | Limited by staff | Scales with volume |

| Compliance | Risk of manual errors | Built-in compliance rules |

| Customer communication | Phone calls, letters | Automated SMS, email, WhatsApp |

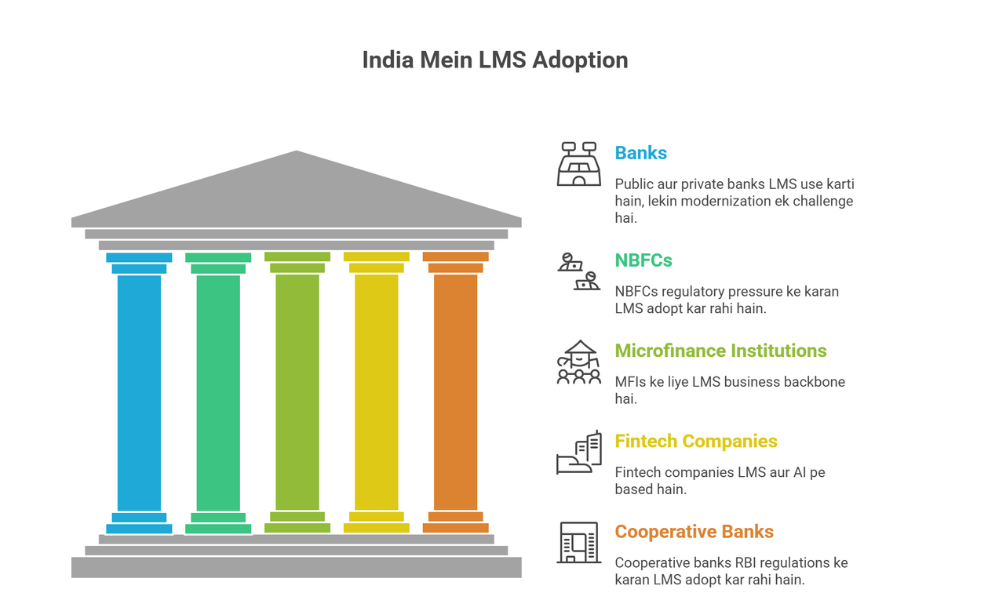

India Mein LMS Kaun Use Karta Hai?

Banks

Public sector aur private banks dono ke paas LMS hota hai, usually core banking system ke saath integrated. State Bank of India, HDFC Bank, ICICI Bank — sab ke paas robust loan management infrastructure hai. Lekin zyada tar traditional banks ne systems decades pehle implement kiye the aur unhe modernize karna ek badi challenge hai.

NBFCs (Non-Banking Financial Companies)

India mein 10,000 se zyada registered NBFCs hain. In mein se bahut saari companies pehle Excel aur manual processes pe chal rahi thi. Ab regulatory pressure aur competition ke chalte LMS adoption mandatory sa ho gaya hai. Bajaj Finance, Muthoot Finance, aur Mahindra Finance jaisi companies apne proprietary LMS use karti hain.

Microfinance Institutions

Bandhan Bank (pehle Bandhan MFI), SKS Microfinance (ab Bharat Financial), aur hazar se zyada smaller MFIs — inke liye LMS business backbone hai. Field collection, group meetings, aur JLG management sab LMS se handle hota hai.

Fintech Companies

Navi, KreditBee, MoneyTap, CASHe — yeh companies pure digital model pe chalti hain. Unka poora business LMS aur AI-driven underwriting pe based hai. 5 minute mein loan approve karna sirf LMS ke through possible hota hai.

Cooperative Banks aur Credit Societies

Small cooperative banks aur urban credit societies bhi LMS adopt kar rahi hain. RBI ki tighter regulations ne unhe digital hone par majboor kiya hai.

LMS Select Karte Waqt Kya Dekhein?

1. Business Size aur Loan Volume

Ek 50-crore ki MFI ko aur ek 5000-crore ki NBFC ko alag LMS chahiye. Volume, product complexity, aur geographic spread ke hisaab se system choose karo.

2. Cloud-based ya On-premise?

Cloud-based LMS (SaaS) mein upfront cost kam hoti hai, maintenance vendor karta hai, aur scaling easy hoti hai. On-premise mein data control zyada hoti hai lekin IT infrastructure maintain karna padta hai. Chhoti companies ke liye cloud better hai; agar sensitive data control aur customization zyada chahiye toh on-premise consider karo.

3. Customization ki Zaroorat

Har lending business unique hota hai. LMS ko aapki specific loan products, interest rate structures, aur collection policies ke saath kaam karna chahiye. Ek rigid, one-size-fits-all system long term mein headache ban jaata hai.

4. Integration Ecosystem

Pehle se existing systems kaun se hain? Core banking, accounting software, CRM — inke saath LMS integrate hona chahiye. API documentation achha hona chahiye aur integration support available hona chahiye.

5. RBI aur Regulatory Compliance

India-specific compliance features chahiye. Fair Practice Code adherence, KYC norms, CERSAI integration (for mortgage loans), aur GST calculations — yeh sab out-of-the-box milne chahiye.

6. Vendor Track Record

LMS ek long-term investment hai. Vendor ka financial stability, client list, aur support quality dekhna zaroori hai. References lo — existing clients se baat karo.

7. Total Cost of Ownership

Sirf license cost mat dekho. Implementation cost, training cost, customization cost, aur annual maintenance charges — sabko add karo toh actual TCO samjh aata hai.

Loan Management System mein AI aur Automation ka Role

2026 mein LMS sirf software nahi raha — yeh increasingly intelligent ho gaya hai.

AI-based Credit Scoring

Traditional Credit score ke saath alternate data use ho rahi hai. Bank statement analysis, social media behavior (kuch countries mein), GST data, aur psychometric assessments — AI in sab ko combine karke better credit decisions le raha hai, especially thin-file customers ke liye jo formally credit history nahi rakhte.

Automated Collections aur Recovery

AI call bots EMI reminders dete hain. Propensity-to-pay models predict karte hain kaunsa customer kis channel pe respond karega. Isse human collectors ko sirf high-risk cases pe focus karna padta hai, productivity 3x ho jaati hai.

Fraud Detection

Real-time fraud detection algorithms loan application ke time hi suspicious patterns identify karte hain. Fake documents, identity theft, aur synthetic fraud — AI yeh sab traditional rule-based systems se zyada accurately detect karta hai.

Chatbot-based Customer Service

Loan status, outstanding balance, foreclosure amount — customer yeh sab khud chatbot se puch sakta hai 24 ghante, bina branch jaaye.

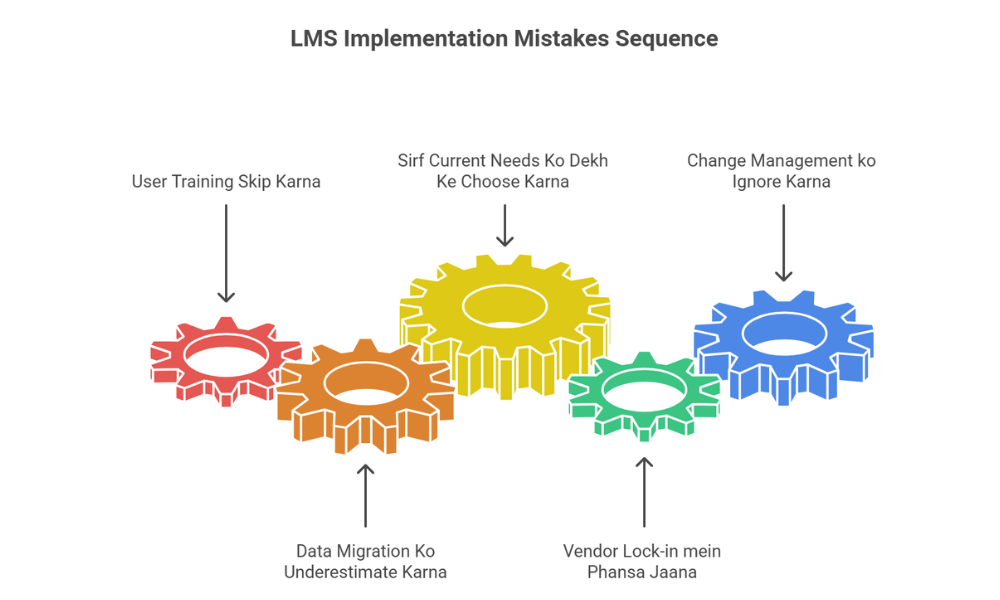

LMS Implementation: Common Mistakes Jinse Bachna Chahiye

Mistake 1: User Training Skip Karna

Bahut saari companies best LMS buy karti hain aur phir poorly implement karti hain kyunki staff ko theek se train nahi kiya jaata. System sirf utna achha hota hai jitna achha log use karte hain.

Mistake 2: Data Migration Ko Underestimate Karna

Purana data (Excel files, physical registers) naye system mein migrate karna ek massive task hai. Time aur resources iske liye alag se plan karne chahiye.

Mistake 3: Sirf Current Needs Ko Dekh Ke Choose Karna

Aaj aapka portfolio 100 crore ka hai, 2 saal baad 500 crore ka ho sakta hai. Ek LMS jo scale nahi kar sakta woh dobara implementation force kar deta hai.

Mistake 4: Vendor Lock-in mein Phansa Jaana

Kuch vendors proprietary formats use karte hain jisse data export karna mushkil ho jaata hai. Always data portability aur open APIs ki condition rakhni chahiye contract mein.

Mistake 5: Change Management ko Ignore Karna

LMS implement karna sirf technical project nahi hai — yeh organizational change hai. Staff resistance common hai. Change management aur internal communication zaroori hai.

Conclusion: Kya Aapko LMS Chahiye?

Agar aap ab bhi Excel pe loan portfolio manage kar rahe hain, manually EMI reminders bhej rahe hain, ya audit ke liye raat bhar data nikalne mein lage hain — toh jawaab clear hai.

Haan, aapko Loan Management System chahiye.

Lending business mein competition tez ho raha hai. Customers ki expectations badh rahi hain. Regulatory scrutiny increase ho rahi hai. Aur data-driven decisions lene ki capability aapke competitors ke paas agar hai aur aapke paas nahi, toh gap waqt ke saath badhta hi jayega.

LMS sirf ek software tool nahi hai. Yeh aapke lending operations ka foundation hai.

Sahi system choose karo, sahi implement karo, aur sahi use karo — aur yeh investment returns multiple times deta hai.

GrInTech India fintech aur lending technology pe focused content aur solutions provide karta hai. LMS selection, implementation, aur optimization ke baare mein agar koi specific help chahiye toh hamse contact karein.

1 reply on “Loan Management System: Complete Guide In 2026”

I appreciate how genuine your writing feels. Thanks for sharing.