A complete step-by-step guide to loan software migration, covering migration planning, data migration, validation & testing, downtime control, and a post-migration checklist for seamless fintech implementation.

Introduction Of Loan Software Migration

Loan software migration is no longer a technical upgrade it’s a strategic move. As lending becomes more digital, regulated, and customer-driven, financial institutions can’t afford to rely on outdated systems. Whether you’re running an NBFC, microfinance institution, or consumer lending business, a well-planned loan software migration can dramatically improve operational efficiency, compliance readiness, and borrower experience.

But let’s be honest migration can feel risky. Concerns about data loss, downtime, integration failures, and compliance gaps are real. The good news? With the right approach, migration can be smooth, structured, and highly rewarding.

In this guide, we’ll walk through each step of a successful migration from planning to post-go-live optimization, so your transition is seamless and future-ready.

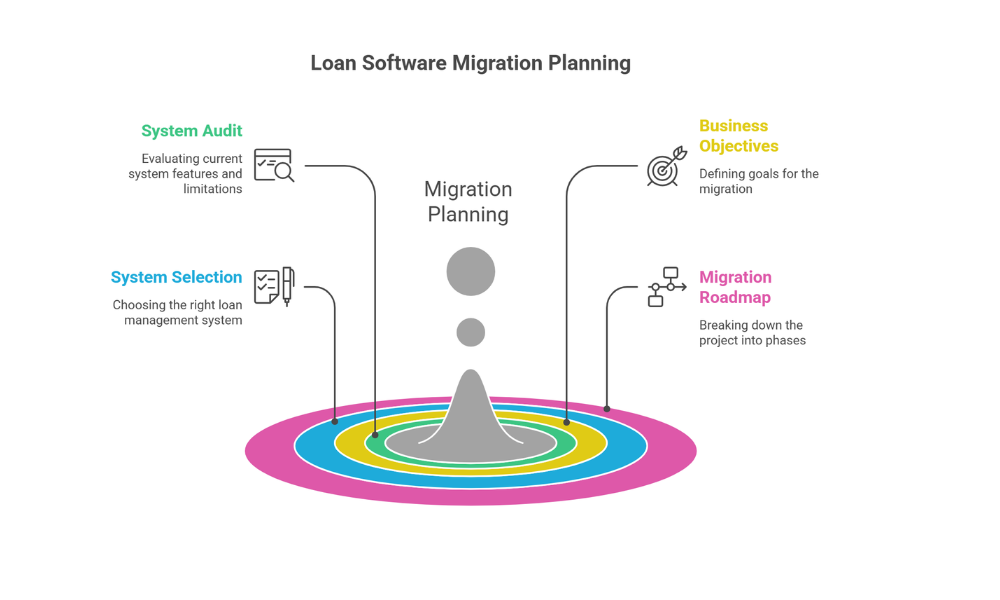

Migration Planning

Every successful loan software migration begins with strategic planning. Rushing this phase often leads to unexpected costs and operational disruption.

1. Audit Your Current System

Start with a complete system audit:

- What features are you currently using?

- Which workflows are manual?

- Where do bottlenecks occur?

- Are you facing compliance or reporting limitations?

This stage is essential in any legacy system migration because it highlights inefficiencies and sets a benchmark for improvement.

Look beyond features. Evaluate:

- Database structure

- Integration capabilities

- API readiness

- Security standards

- Scalability limitations

If your current platform struggles with real-time loan tracking, automated underwriting, credit bureau integrations, or regulatory reporting, it’s a clear signal that modernization is overdue.

2. Define Business Objectives

Migration should support business growth, not just technical replacement.

Common goals include:

- Faster loan disbursement cycles

- Improved EMI tracking

- Reduced NPA risk

- Automated compliance reporting

- Better customer self-service portals

Align your fintech implementation roadmap with measurable KPIs such as reduced TAT (Turnaround Time), lower operational cost per loan, and improved portfolio performance.

3. Choose the Right Loan Management System

When evaluating vendors, consider:

- Cloud-based vs on-premises architecture

- Customization flexibility

- Integration with payment gateways, credit bureaus, eNACH, UPI, and accounting systems

- Regulatory compliance capabilities

- Data security certifications

A modern loan management platform should support loan origination, underwriting, servicing, collections, and reporting within a unified ecosystem.

4. Create a Migration Roadmap

Break the project into phases:

- Requirement gathering

- Data mapping

- System configuration

- User acceptance testing (UAT)

- Go-live

- Post-go-live monitoring

Assign responsibilities clearly between internal stakeholders and the implementation partner. Establish timelines and define escalation paths for risk mitigation.

Data Migration

Data migration is the backbone of any loan software migration. If data integrity fails, the entire system becomes unreliable.

1. Data Assessment & Cleanup

Before migration, cleanse your data:

- Remove duplicate borrower profiles

- Correct incomplete KYC details

- Standardize loan product codes

- Validate repayment schedules

This reduces complications during import and ensures better analytics after go-live.

2. Data Mapping

Data mapping ensures every field in your legacy system aligns correctly with the new platform.

For example:

- Borrower ID → Customer Master ID

- Loan Account Number → Loan Reference Code

- Repayment Schedule → EMI Structure

Errors in mapping can disrupt amortization schedules and portfolio calculations. Take this stage seriously.

3. Secure Data Transfer

Use encrypted transfer protocols and follow regulatory data protection norms. Financial institutions must comply with data privacy standards to prevent breaches during legacy system migration.

Validation & Testing

After migrating data, validation is critical.

1. Parallel Run Testing

Run both systems simultaneously for a defined period:

- Compare repayment entries

- Check interest calculations

- Validate outstanding balances

- Confirm NPA tagging logic

This ensures your new platform reflects accurate financial positions.

2. User Acceptance Testing (UAT)

Involve:

- Operations teams

- Credit managers

- Finance teams

- Compliance officers

Let them test real-world workflows—loan disbursement, EMI posting, foreclosure, restructuring, and reporting.

Collect feedback and fix issues before final go-live.

3. Compliance Testing

Verify:

- Regulatory reports

- Audit trails

- Data access controls

- Customer communication logs

Strong validation protects your institution from regulatory risks.

Downtime Control

One of the biggest fears during loan software migration is operational downtime.

1. Plan Go-Live Timing Strategically

Avoid:

- Month-end closing periods

- High collection days

- Regulatory reporting deadlines

Choose a low-activity window for final cutover.

2. Backup Everything

Maintain:

- Full database backups

- Incremental backups

- Rollback strategy

If something fails, your business should continue uninterrupted.

3. Staff Training Before Go-Live

Even the best fintech implementation fails if users are unprepared.

Provide:

- Hands-on training

- Workflow manuals

- Troubleshooting guides

Confidence reduces errors during the transition phase.

Post-Migration Checklist

Going live is not the finish line. It’s the beginning of optimization.

Here’s a structured post-migration checklist:

1. Performance Monitoring

Track:

- System response time

- EMI posting accuracy

- Disbursement workflow efficiency

- Report generation speed

2. Data Reconciliation

Reconcile:

- Outstanding loan balances

- Accrued interest

- Collection data

- GL integrations

Ensure financial statements remain accurate.

3. Customer Communication

Inform borrowers about:

- New repayment portals

- Updated payment references

- Customer support changes

Clear communication avoids confusion and missed payments.

4. Continuous Optimization

A modern loan management system offers analytics dashboards. Use them to:

- Track delinquency trends

- Analyze portfolio risk

- Improve underwriting criteria

- Automate collection reminders

Migration should unlock strategic insights, not just operational improvements.

Common Challenges in Loan Software Migration

Understanding potential risks helps you prepare better:

- Incomplete data mapping

- Integration failures with third-party APIs

- Resistance from internal teams

- Underestimated migration timelines

- Poor change management

Address these proactively through structured governance and regular progress reviews.

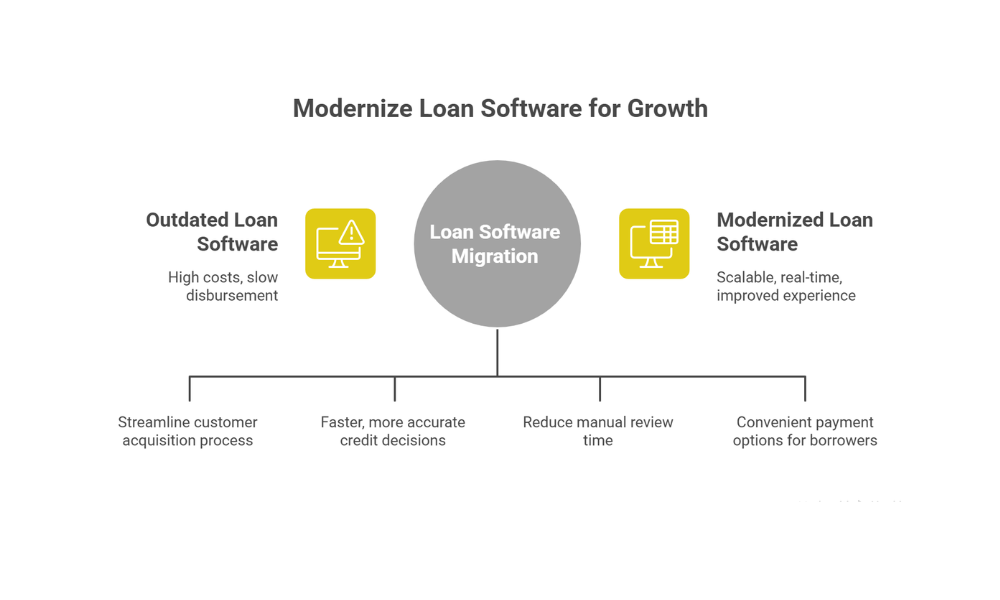

Why Modernizing Matters More Than Ever

The lending industry is evolving rapidly. Digital onboarding, instant credit scoring, automated underwriting, and mobile repayment platforms are becoming standard expectations.

Institutions that delay loan software migration risk:

- Higher operational costs

- Compliance penalties

- Slower disbursement cycles

- Reduced customer satisfaction

On the other hand, lenders who modernize benefit from:

- Scalable infrastructure

- Real-time portfolio visibility

- Better risk management

- Improved borrower experience

Conclusion: Make Your Migration a Growth Strategy

A successful loan software migration is not just about replacing old technology—it’s about building a stronger, smarter lending operation.

With proper migration planning, structured data migration, rigorous validation & testing, controlled downtime, and a thorough post-migration checklist, your institution can transition confidently into a more agile and compliant future.

If your current system is slowing down growth or limiting innovation, now is the time to act. Start by auditing your existing setup, define your strategic goals, and partner with a reliable fintech implementation team that understands the nuances of lending operations.

The sooner you modernize, the sooner you unlock efficiency, scalability, and long-term competitive advantage.

Ready to begin your loan software migration journey? The next phase of growth starts with a single strategic decision.