Is it time to upgrade loan management software? Discover the clear signs your NBFC has outgrown its current system, including legacy loan system issues, compliance risks, and when to plan your NBFC software upgrade for scalable growth.

If your NBFC is growing but your system feels stuck in the past, it may be time to upgrade loan management software. Many lending businesses expand their portfolio, add branches, and increase disbursements but continue operating on outdated platforms. Over time, legacy loan system issues start slowing everything down: manual errors increase, compliance becomes stressful, and teams spend more time fixing problems than serving customers.

An NBFC software upgrade is no longer just about convenience. It’s about protecting your portfolio, staying compliant with regulations from the Reserve Bank of India, and building a scalable digital lending operation.

Let’s break down the real warning signs that your loan software is holding you back.

Operational Warning Signs

Growth should feel exciting. But if growth feels chaotic, your system might be the problem.

1. Too Much Manual Work

If your team is still managing loan approvals, EMI tracking, or NPA calculations in spreadsheets, your system lacks automation. Modern loan lifecycle management software should handle:

- Automated EMI schedules

- Real-time loan tracking

- Digital loan disbursement

- Automated reminders and collections

Manual processes increase human error, slow down turnaround time, and frustrate both staff and borrowers.

2. Slow Loan Processing

Are approvals taking longer than competitors? Customers today expect quick decisions. A cloud-based loan management system can streamline underwriting and reduce delays. If your system struggles with real-time data or requires multiple logins across platforms, it’s a major bottleneck.

3. Poor Reporting & Limited Insights

If management cannot access real-time portfolio dashboards or risk analytics, decision-making becomes guesswork. Modern NBFC software provides:

- Centralized loan portfolio dashboards

- Automated NPA tracking

- Custom compliance reports

- Branch-wise performance analytics

Without accurate data, risk assessment becomes reactive rather than proactive.

4. Integration Problems

Legacy systems often fail to integrate with CRMs, payment gateways, credit bureaus, or accounting software. API-based lending platforms allow seamless integration. If your team is exporting and importing files manually, it’s a clear sign your system needs modernization.

Risks of Legacy Systems

Legacy loan system issues go beyond operational inefficiency. They create real financial and legal risks.

Older platforms were built for a different era when loan volumes were smaller, and compliance requirements were simpler. Today, digital lending requires agility, automation, and strong cybersecurity.

Compliance Issues

Regulatory compliance is non-negotiable for NBFCs. Guidelines from the Reserve Bank of India evolve regularly, especially in areas like digital lending, data security, and fair practices.

If your system cannot:

- Generate RBI-compliant reports instantly

- Track customer consent records

- Maintain secure borrower data

- Audit loan histories efficiently

you are exposed to regulatory penalties.

Compliance challenges in legacy lending systems often arise because updates require custom coding or vendor intervention. A modern NBFC software upgrade offers built-in compliance modules and automatic updates aligned with regulatory changes.

Security is another concern. Outdated loan servicing platforms may lack encryption standards and advanced authentication. In an age of rising cyber threats, security vulnerabilities in legacy financial systems can damage your reputation overnight.

Scalability Limits

As your NBFC grows, your system should grow with you.

But legacy systems often have scalability problems:

- Limited user access

- Slow performance with high transaction volumes

- Difficulty managing multi-branch operations

- Inability to support new loan products

If launching a new loan scheme requires weeks of configuration, your system is limiting innovation.

Modern SaaS loan management software in India offers cloud infrastructure that handles higher loads effortlessly. Whether you’re managing consumer loans, microfinance, or group lending, scalability should never be a concern.

An upgrade loan management software decision becomes essential when technology starts controlling growth instead of enabling it.

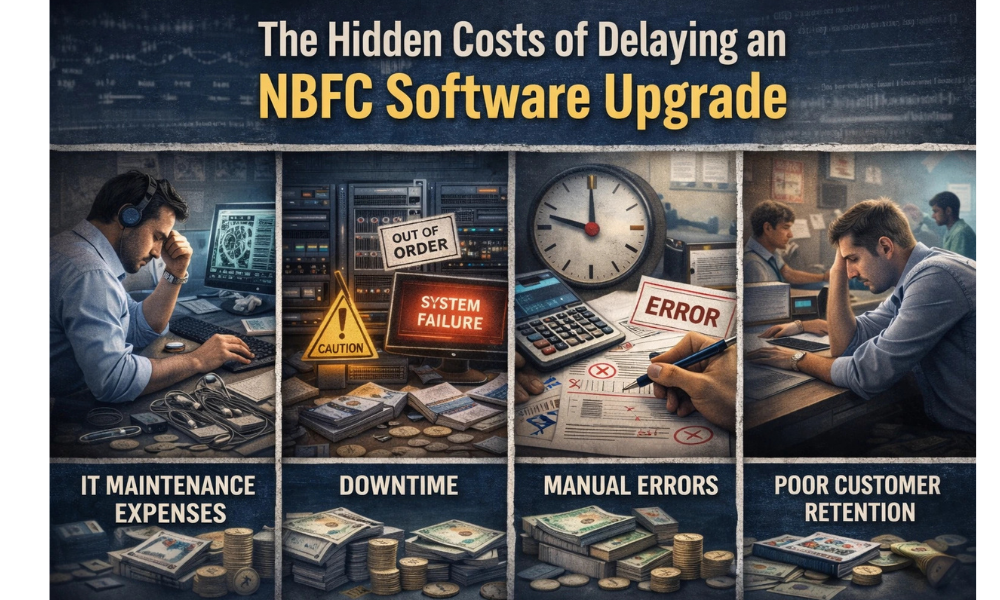

The Hidden Costs of Delaying an NBFC Software Upgrade

Many NBFCs postpone upgrading because they fear migration complexity or cost. But the hidden costs of maintaining legacy systems are often higher:

- IT maintenance expenses

- Frequent downtime

- Manual reconciliation errors

- Delayed collections

- Poor customer retention

According to digital transformation research by McKinsey & Company, organizations that modernize core systems improve operational efficiency and reduce long-term costs significantly.

Sticking to outdated technology might seem cheaper today, but it reduces competitiveness in the long run.

Upgrade Decision: When Is the Right Time?

So how do you know it’s finally time to upgrade loan management software?

Ask yourself these questions:

- Are we struggling to manage compliance updates?

- Is our loan processing slower than competitors?

- Are we facing frequent data inconsistencies?

- Do we lack real-time risk visibility?

- Is IT maintenance consuming too much budget?

If you answered “yes” to even two or three of these, your NBFC has likely outgrown its system.

What a Modern System Should Offer

When planning an NBFC software upgrade, look for:

- End-to-end loan lifecycle management

- Automated underwriting and credit scoring

- Cloud-based infrastructure

- API integrations

- Multi-branch support

- Advanced reporting & dashboards

- Built-in RBI compliance features

- Secure data encryption

Migration today is far smoother than before. With proper data migration planning, downtime can be minimal, and long-term benefits far outweigh temporary adjustments.

Final Thoughts: Don’t Let Technology Slow Your Growth

Every growing NBFC reaches a turning point. The early system that once supported your operations may now be the biggest obstacle.

Legacy loan system issues do not fix themselves. They grow quietly increasing risk, slowing productivity, and affecting customer trust.

Choosing to upgrade loan management software is not just a technical decision. It’s a strategic move toward scalability, compliance, efficiency, and competitive advantage.

If your NBFC is planning expansion, launching new products, or aiming for stronger regulatory alignment, now is the time for an NBFC software upgrade.

Don’t wait for compliance penalties or operational breakdowns to force the decision.

Take control. Modernize your lending operations. Upgrade your loan management software today and build a system that supports your future growth, not limits it.

Frequently Asked Questions

1. When should an NBFC upgrade loan management software?

An NBFC should upgrade loan management software when it starts experiencing operational delays, manual workarounds, compliance challenges, integration issues, or scalability limitations. If your system cannot support growing loan volumes, new product launches, or updated regulatory norms from the Reserve Bank of India, it is time to consider an NBFC software upgrade.

2. What are common legacy loan system issues?

Common legacy loan system issues include:

- Manual EMI calculations

- Slow loan processing

- Poor reporting and limited dashboards

- Integration challenges with credit bureaus and payment gateways

- Security vulnerabilities

- High maintenance costs

These problems reduce operational efficiency and increase compliance risks.

3. How does upgrading loan management software improve compliance?

Modern systems are designed with built-in compliance workflows, automated regulatory reporting, audit trails, and real-time data validation. This reduces the risk of manual errors and ensures adherence to updated NBFC norms issued by the Reserve Bank of India.

4. What are the benefits of a cloud-based NBFC software upgrade?

A cloud-based loan management system offers:

- Scalability for growing loan portfolios

- Real-time portfolio monitoring

- Automated EMI tracking

- Secure data storage

- API-based integrations

- Lower infrastructure costs

It ensures your lending operations remain flexible and future ready.

5. Is data migration risky during a loan management software upgrade?

With proper planning, data migration is manageable and secure. A structured migration process includes data cleansing, mapping, validation, testing, and phased deployment to ensure business continuity during the upgrade.